Empyrean Energy - Hitting the Gas

|

Although Empyrean’s

interest is small in

percentage terms the potential rewards are considerable for a

small company

If you are looking for an exciting investment you need look no further than the Oil & Gas exploration companies listed on AIM. However, with nearly 100 of these companies listed, there are quite a few to choose from.

We have selected Empyrean Energy for our analysis this month. We believe that the company is particularly worthy of further investigation for a number of reasons:-

- The company is having significant drilling success at their Sugarloaf project

- There will be a steady flow of news to interest investors for months and years to come

- All of Empyrean’s four major projects are in politically stable countries (3 in the USA and 1 in Germany)

- ...and all four are onshore

I spoke to Tom Kelly, Director and Co-Founder of Empyrean, by telephone - Tom was in Perth, Western Australia. We discussed Empyrean’s projects and their prospects. In our conversation I learned just how key Empyrean’s Sugarloaf project could be for the company and its shareholders. Unlike some projects Sugarloaf is not a short term thing. Forecasts are indicating the potential for over 40 years of production here. Before I expand on the Sugarloaf project I will firstly say a little about the company’s brief history.

Change of Focus

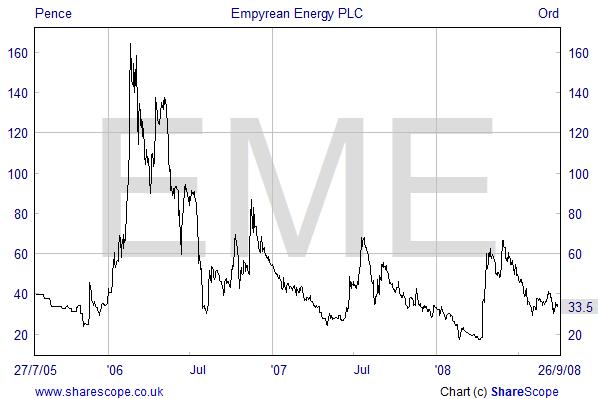

Empyrean (meaning: The highest heaven, where the pure element of fire was supposed by the ancients to subsist) was first listed on AIM just over 3 years ago. At that time the company raised £2.1 million in a placing at 35p per share. These funds were raised to progress the company’s German gas project located near Frankfurt. As can be seen from the graph below, the shares have had a number of upward spikes. They even reached £1.60 within their first year of trading but today the shares are not far from the price of the initial placing.

Unfortunately, the first ‘Glantal-1’ well at the German prospect did not encounter commercial quantities of gas and subsequently the project has been put on the ‘back burner’ – perhaps an apt place for a gas prospect to be! Nonetheless, Empyrean still believe that this project has a lot of potential.

Empyrean’s focus has subsequently switched to the USA and it is one of the three US projects, namely Sugarloaf, where the current excitement around Empyrean lies. Sugarloaf is an oil and gas project in the Gulf Coast Basin of Texas.

Sugarloaf

The company refer to Sugarloaf as a multi Trillion cubic feet gas prospect and that is an awful lot of gas. To date, all 7 of the wells that have been drilled have encountered gas in varying quantities. Most of the wells have been fracture stimulated (what’s that? – see here) with varying results. As yet, very little gas is being produced, but some of the wells are likely to be significant producers. Sugarloaf has the advantage of a nearby gas pipeline infrastructure so it will be easy to sell the gas once the wells are producing.

Empyrean has a working interest in a 16 well program that commenced in 2007. Empyrean’s actual interest ranges from 7.5% to 18% - see the RNS here from May 2007 for more details of Empyrean’s interest in this area. This RNS is also useful in understanding the split of Sugarloaf into 2 Blocks (A & B) with differing operators. One of the operators is a major international oil and gas company whose name is ‘undisclosed for confidentiality purposes and to preserve and protect competitive advantage’ – the company is named on numerous different bulletin boards worldwide and as such is not the world’s best-kept secret.

Although Empyrean’s interest is small in percentage terms, the potential rewards are considerable for a small company (market cap £20m at 34p) . It is almost exactly 2 years ago since the company reported the ‘encouraging gas shows’ from a 92 feet gas pay in the first Sugarloaf well. To see a current status of the 7 wells drilled to date we would recommend the ADVFN ‘Long Term Investors Thread’ bulletin board – see here (if you are not already registered for advfn, click the link anyway and then select ‘cancel’ – you will then be able to register for advfn for free).

The vertical wells drilled at Sugarloaf have encountered 3 potential pay zones – referred to as the upper, middle and lower zones. To date, results from the upper zone have been by far the most encouraging. However, the company is hopeful that the lower zones will eventually prove to be commercial.

In a broker’s note dated 23 May 2008, Hoodless Brennan placed an estimated value on Sugarloaf at 74p per share. They say that the figure is based on conservative estimates and is in line with Empyrean’s internal Net Present Value estimate. At this stage, estimates are extremely ‘early stage’. Not only do we not know how much oil and gas is down there, the volatility of the dollar as well as oil and gas prices make long term forecasting even less reliable than usual. Tom Kelly indicated that their new brokers, Blue Oar, are currently working on a new detailed research note.

Prospects at Sugarloaf

The immediate interest at Sugarloaf is the on-going drilling of the Kowalik 1 Horizontal Well. This well is drilling horizontally through a 6000 foot of the upper pay zone. The company reported on September 24 that the well had drilled 'approximately 2,500 ft of the planned 6,000 ft of horizontal section within the Austin Chalk’. The company also reported sustained gas flaring during drilling. However the company cautioned that: ‘whilst encouraging, the commercial significance of these gas shows and flares will not be known until the well has been flow tested’. To read the 24 September RNS statement click here. We shall be looking out for the flow test results in a few weeks time. This well is particularly important for Empyrean as they have an 18% interest in the well.

I asked Tom Kelly when we would see production begin in earnest at Sugarloaf. Tom was unable to give an exact timetable as there are too many variables, but he indicated that the operator is working as quickly as possible to get the first two Block A wells into production. Tom explained that Empyrean are fortunate that wells at Sugarloaf have produced a good deal of gas condensate (what’s that? – read about condensate on Wikipedia). The advantage of condensate is that it will be financially rewarding with its price being close to that of oil. Also, condensate is easy to store and transport by truck. Permanent production facilities for gas/condensate separation are currently being built.

As yet the middle and lower pay zones have not been proved to be commercial. However, Tom believes that there is ‘tremendous potential for the middle and lower pay zones to produce at commercially attractive flow rates’ and he suspects that it will not be long before ‘further work will be undertaken in this regard’.

Other Projects

Sugarloaf has been taking centre stage over recent months, but Empyrean's three remaining projects have all got potential:-

- Glantal, Germany – The first well in 2006 did not find commercial quantities of gas. Empyrean, who have a 52% interest, reported in February 2008 that they are working with the operator to finalise plans for a seismic program to assist in the definition of further drill targets. The timing here will depend on the availability of a seismic team. The company still believe that there could be a very large opportunity gas field here.

- Eagle Project, California – A well was drilled here in 2005/6 and oil was encountered, but due to technical difficulties the well was abandoned. In a February 2008 RNS the company reported:

‘The operator, ASX Listed, Victoria Petroleum Ltd ('VicPet') has been attempting to farm down their interest in this project and attract a new locally based (USA) operator in to operate.

We are aware that the project was showcased in Houston during the last fortnight at a major US oil conference and that there has been significant interest in the project.

Empyrean currently maintains their 38.5% interest in this project and keenly awaits news of any negotiations with the operator such that a new well can be drilled on this project as early as possible.’

Given there has been little activity here for a while you could be forgiven for thinking that the prospects cannot be too exciting. However, Hoodless Brennan in their May note attribute a value of 67p per share to this project.

- Margarita, Texas - Six shallow wells were drilled here in 2007. Three of these found commercial quantities of oil and gas and are now providing useful cash flow for Empyrean. The quantities here are not that significant and Hoodless Brennan put a value of 5.9p per share on Margarita.

Finances

In June 2008 Empyrean raised just over £4 million in a placing at 50p per share. This was said to be for funding development at Sugarloaf. With the high cost of drilling and fracture stimulation work at Sugarloaf these funds could be spent fairly quickly and Empyrean will be keen to see some significant production revenue soon.

It is interesting to note that a new Broker and Nomad in Blue Oar were appointed in August 2008. Also, a new Non-Executive Finance Director was appointed in the same month.

Investment case

Investment in small Oil & Gas exploration companies can be extremely risky. The rewards can be huge but so can the potential for losses. Having said that, where an exploration company can successfully transform itself from an explorer to a producer there can be considerable potential for share price improvement.

The risks of investing in exploration companies have increased recently because of the credit crunch and the difficulty in raising capital. This factor and the fall in oil prices in recent weeks have caused considerable weakness in the share prices of junior oil & gas exploration companies. For example, despite drilling successes, Empyrean’s share price has fallen by nearly 50% from its 2008 high at the end of May this year.

You could argue that the spot price of oil today should have little impact on the average price that Empyrean will receive for its Gas and Oil over many years of production. However, the share price and sentiment around companies such as Empyrean are greatly influenced by the oil price. If you believe that oil and gas prices have significantly further to fall in the short to medium term then you may be best to avoid this sector completely for a while.

Empyrean are certainly involved in a very significant project with Sugarloaf and it could be huge. Exactly how big it will be is uncertain and the delay in finalising development of some of the more successful exploration wells does not help investors in their understanding of the potential here. A new detailed research note is expected shortly from Blue Oar and it is hoped that this will help investors to gain a better understanding of the potential value in Sugarloaf.

A cautious investor may wish to see positive cash flow and more evidence of the potential of Sugarloaf before considering investment here. However, waiting for this could mean paying a much higher price for shares. Empyrean is an actively traded share and the share price can be volatile when drilling news is expected and released. In the weak market conditions recently, the share price has tended to fall back once the excitement of drilling news has faded.

Aimzine will provide updates on Empyrean over the coming months.

Written by Michael Crockett, Aimzine

tremendous potential

for the middle and

lower pay zones